The Great Real Estate Debate: Public vs. Private

Stocks and bonds often get the spotlight among investors, but real estate can also play a valuable role in long-term asset allocations.

For example, real estate and rental income may help provide a long-term hedge to running inflation. Income derived from real estate investments may help investors fund spending needs over time or contribute to long-term growth objectives in combination with property value appreciation.

Real estate can also provide diversification benefits in a total portfolio as it can behave differently, exhibiting different return patterns than stocks and bonds.

What Are REITs?

Real estate investment trusts (REITs) are a common way to gain exposure to real estate investments. First established in 1960 under the Eisenhower administration, REITs are companies that own or finance income-producing real estate but act as passthrough vehicles that distribute income to shareholders.

Companies operating as REITs don’t pay taxes on the earnings they distribute to shareholders, like mutual funds and ETFs. For a company to enjoy the benefits of the REIT structure, U.S. regulations set certain requirements that include:

75% of assets in real estate assets or cash-like securities.

75% of taxable income from real estate-related income like rent on a property, mortgage interest, gains on the sale of property and dividends/gains from other REITs.

90% or more of ordinary income and 95% of net capital gains delivered to shareholders.

Accessing Diversified Real Estate Exposure

REITs expand opportunities for everyday investors to pursue broadly diversified real estate investments. While many investors may own property through their primary residences, REITs can provide exposure to many different property types in various locales, such as single-family rentals, hotels and resorts, office buildings, storage facilities, retail shopping malls and industrial facilities.

As of the end of 2020, some 250 U.S. REITs collectively owned more than 500,000 properties totaling $2 trillion in value.1

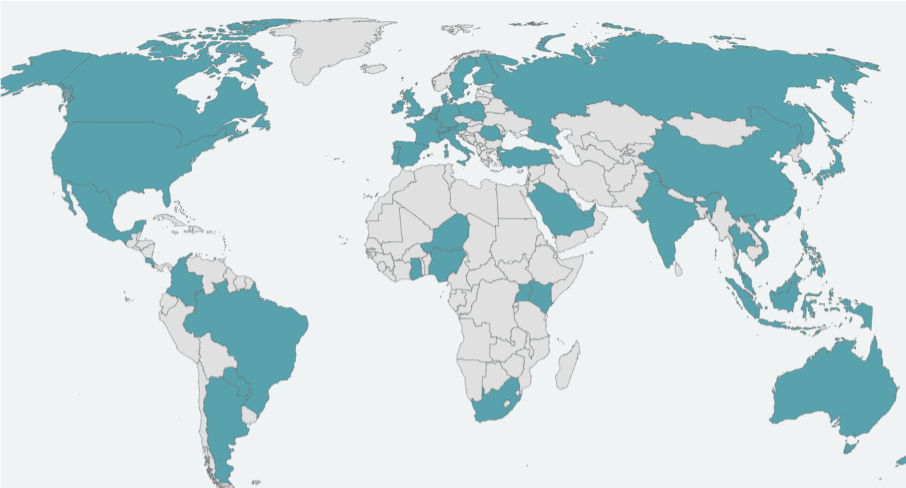

The U.S. approach to REITs has also served as a model for many other countries to create similar securities. Hundreds of public REIT-like companies operate outside the U.S., offering exposure to properties in more than 50 countries worldwide.

Figure 1 | Global REITs Offer Exposure to Properties in Over 50 Countries

COUNTRIES WHERE REITS OWN PROPERTY

Source: Avantis Investors, data from Bloomberg.

How Do Public and Private REITs Differ?

Most REITs are publicly traded on stock exchanges. Investors can purchase shares of individual REITs or invest through commingled funds like ETFs and mutual funds that invest in REITs. Mutual fund and ETF investors do not own shares of REITs directly.

REITs can also operate as private companies that don’t register with the U.S. Securities and Exchange Commission (SEC) or trade on stock exchanges. Private REITs are typically available only to institutional or accredited investors.

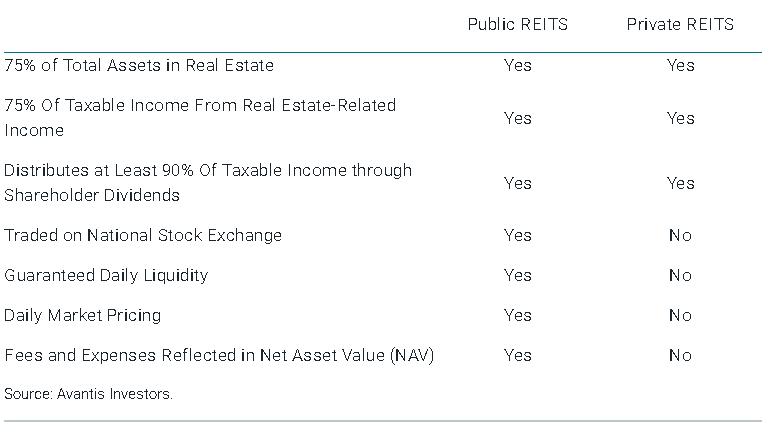

Figure 2 lays out other similarities and differences. To start, to operate as either a public or private REIT, a company must meet the criteria required to qualify as a REIT. For both public and private REITs, this means the majority of total assets must be invested in real estate, and the bulk of income must be passed through to shareholders as dividends. In other words, the underlying exposure may be similar.

Figure 2 | Comparing Key Attributes of Public and Private REITs

Comparing Key Attributes of Public and Private REITs

Beyond these required features of REITs, we see two clear differences between public and private REITs.

Liquidity: Because private REITs aren’t traded in a public market, they offer no guarantee of daily liquidity to shareholders. They are often considered illiquid investments. In contrast, public REITs can generally be bought and sold daily in the public market.

Pricing: Public REITs are priced each day as buyers and sellers transact in the market, reflecting the market’s current expectations of the underlying properties’ valuations, expected cash flows from rental income, and costs from expenses and management fees. Private REITs rely on appraisal-based pricing, meaning a REIT’s net asset value (NAV) is based on underlying property values that are often estimated quarterly or sometimes less frequently, and unlike public REITs do not reflect management fees and expenses.

One risk for investors to consider when evaluating private REITs is that appraisal-based pricing may mean private REIT prices are stale or, in other words, don’t reflect current information that could affect prices. Another risk comes from the price of private REITs not reflecting fees and expenses.

Let’s consider an example to compare market pricing versus appraisal-based pricing. Imagine two REITs (REIT 1 and REIT 2) that share the same properties at an even 50/50 split. REIT 1 has a lower, flat management fee (e.g., 0.50% of assets), and REIT 2 has a higher, flat management fee (e.g., 1% of assets) plus a performance participation fee (e.g., 15% of any appreciation).

If both REITs were priced in the market, REIT 2 should have a lower price than REIT 1. Investors would likely pay less for REIT 2, given that they would also receive less because of the higher fees. If both REITs were priced only by appraisal values, as is the case for private REITs, each would have the same price since the NAV for each REIT is based on the same underlying properties and management fees are not part of the value of the properties.

So, if we paid full price for the properties based on the appraisal-based NAV but only received 85% of the appreciation (as in the case of REIT 2), then this would be like paying full price for only 85% of the properties.

Given these differences in liquidity and transparency in pricing, investors may wonder what drives the appeal of private real estate. It may come from a belief that private real estate can offer higher returns. However, that may not be the case. The differences noted in how private and public REITS are priced as well as typically higher fees to invest in private real estate, may mean investors have a higher hurdle to surpass for private REITs to deliver higher returns than public REITs.

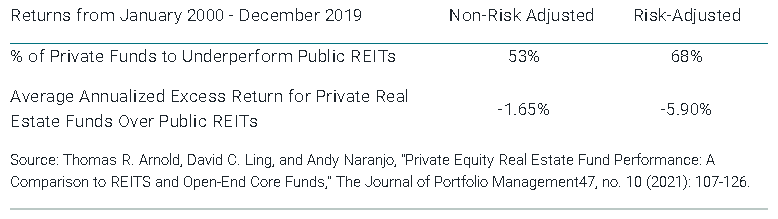

A recent study from The University of Florida explored this topic.2 Researchers compared the estimated final internal rate of return (IRR)3 of 375 U.S. closed-end private real estate funds to the period-matched returns of a U.S. public REITs index over the 20-year period from 2000 through 2019. The authors also estimated risk-adjusted returns in an attempt to account for differences in risk from typically higher leverage and lower liquidity for private real estate funds.

As shown in Figure 3, their results found no observable return advantage for U.S. private real estate funds for the sample studied. Whether adjusting for risk or not, public REITs outperformed more than half of the private real estate funds examined. The average unadjusted return difference for the private funds versus public REITs was -1.65%. The study found similar results for non-U.S. private real estate funds.

Figure 3 | Many Private Real Estate Funds Have Underperformed Public REITs

Many Private Real Estate Funds Have Underperformed Public REITs

We can’t say with certainty what has led private real estate funds to underperform public REITs in this study. However, differences in pricing, as well as differences in the level of fees between private and public funds, may play a role.

What’s important is that investors understand the potential benefits, risks and tradeoffs between investment options and make decisions they believe best meet their unique investment goals.

But if the objective is gaining broadly diversified real estate exposure, public REITs, or funds that invest in public REITs, can be an efficient way to get it and one we believe may meet the mark for many investors.

1 Source: National Association of Real Estate Investment Trusts (Nareit).

2 Thomas R. Arnold, David C. Ling, and Andy Naranjo, “Private Equity Real Estate Fund Performance: A Comparison to REITs and Open-End Core Funds,” The Journal of Portfolio Management 47, no. 10 (2021): 107-126.

3 Internal rate of return (IRR) is the projected annual compound growth rate of a specific investment over time.

The opinions expressed are those of American Century Investments and are no guarantee of the future performance of any American Century Investments portfolio.

This material has been prepared for educational purposes only and is not intended as a personalized recommendation or fiduciary advice. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

Diversification does not assure a profit nor does it protect against loss of principal.

Past performance is no guarantee of future results.

FOR FINANCIAL PROFESSIONAL USE ONLY/NOT FOR DISTRIBUTION TO THE PUBLIC