Take It to the Bank

Over the last month, basketball fans have enjoyed the “madness” of the NCAA tournament, which has certainly lived up to its branding. At the same time, the banking industry delivered “madness” and uncertainty of its own.

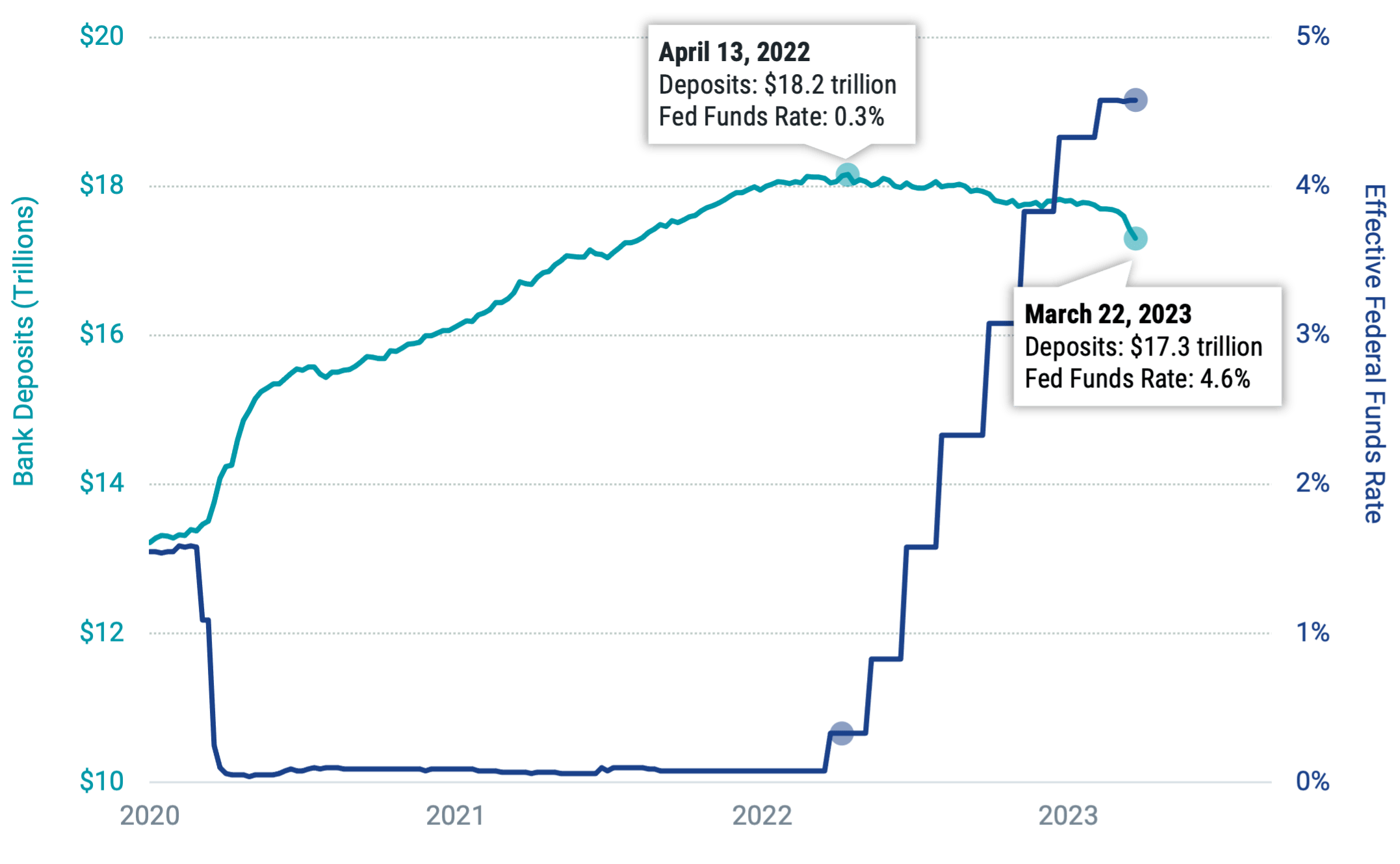

With the recent and widely reported fall of Silicon Valley Bank and Signature Bank, we are now seeing, perhaps, the first real challenges to emerge from the Federal Reserve’s (the Fed’s) rate campaign against inflation. In Figure 1, we observe that U.S. bank deposits soared after the onset of the COVID-19 pandemic in early 2020, spurred by a combination of factors that included government stimulus increasing household incomes, households holding more cash in the face of low interest rates and volatile markets, and businesses drawing cash from lines of credit for precautionary capital.¹

Figure 1 | U.S. Bank Deposits and the Effective Federal Funds Rate

Data from 1/1/2020 – 3/22/2023. Source: Board of Governors of the Federal Reserve System, Federal Reserve Bank of New York. The Federal Funds Rate is the interest rate at which depository institutions, such as banks and credit unions, lend and borrow funds from each other on an overnight basis to maintain their reserve requirements. References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. As of March 31, none of the funds referenced in this document had exposure to the securities referenced greater than 0.01%.

Shortly after the Fed began raising rates in early 2022 to fight persistent inflation, U.S. bank deposits reached an all-time high (April 2022). Since that time, the Fed Funds Rate has risen sharply to around 5%, and deposit levels have retreated in part due to the opportunity to earn higher yields elsewhere. Over the last month, however, the rate of decline dramatically escalated as fear spread over the safety of deposits (especially those exceeding the FDIC insurance limit of $250K). Nearly $400 billion in deposits left U.S. banks over the 4-week period ending March 22—the largest 4-week decline since the start of 1973.

The concerns that led to depositor anxiety stemmed from the impact of rapidly rising rates on the balance sheets of certain banks. A simple understanding of how banks work sheds light on the matter.

How Banks Work

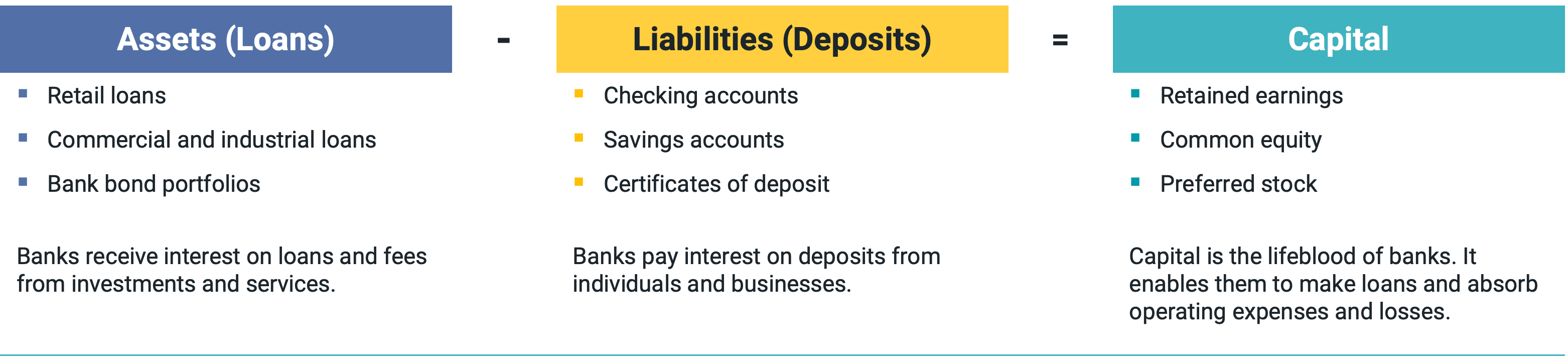

Banks play an important role in the economy. Figure 2 shows how they connect savers and borrowers, a critical function for economic growth.

Figure 2 | Banks Are Critical to a Functioning Economy and Economic Growth

Banks serve as the intermediary between savers and borrowers. Banks take in deposits (liabilities) that are typically held for long periods of time. That allows banks to use that money to lend to individuals and businesses (assets).

The difference between loan rates (what the bank earns) and deposit rates (what the bank pays) is the primary way banks generate earnings. Because it takes time to convert deposits to loans, banks may also invest deposits in other generally “safe” investments such as bonds from the U.S. Treasury to earn interest income until that money is needed to serve borrowers.

Bank capital is the difference between a bank’s assets and liabilities. Capital serves an important role as it gives banks the capacity to grow assets (i.e., make more loans) and absorb operating expenses and losses while continuing to provide financial services.

Given the critical importance of banks to the economy and economic growth, they are heavily regulated in order to limit risks of failure and to maintain confidence in the stability of the banking system. In a nutshell, these regulations require banks to maintain minimum levels of high-quality, liquid capital (i.e., can easily be used to raise/deliver cash) relative to total assets.

Through this framework, it’s easy to understand the impact that rising rates may have on banks today. However, the effect can certainly vary depending on the makeup of each individual bank’s balance sheet.

For banks with bonds held on their balance sheet, the current value of those bonds has dropped as rates have risen (bond prices fall as rates rise). This represents unrealized losses for the bank, and as assets go down so does bank capital.*

If deposits are stable, these bonds can be held to maturity, where banks would hypothetically receive face value. However, if many depositors are trying to get their money out at the same time (as was the case for Silicon Valley Bank) then the bank may be forced to sell bonds to raise cash resulting in the realization of losses and depleted capital. So, with stable deposits, the bank may remain viable, but in the face of a bank run the issue compounds.

Welcome News for Depositors

This may all sound like bad news, but the U.S. Treasury, FDIC, and Federal Reserve acted swiftly to try to quell fears of depositors and help banks maintain adequate capital.

First, the government moved to fully protect insured and uninsured deposits at recently failed regional banks. On March 21, Treasury Secretary Janet Yellen added that the government could protect depositors at other banks if needed, offering an additional signal that depositor money should be safe.

Further, the government provided banks with a special lending program that allows banks to source liquidity by posting assets (e.g., bonds) as collateral at face value.

These combined efforts have helped to stem the tide on any immediate bank runs and is likely welcome news for depositors and banks alike. Even more, other banks have stepped in to buy the assets of the failed banks.

What This Means for Investors

For investors, the news from the banking industry has contributed to uncertainty and market volatility. While the S&P 500 Index was positive for the month of March, albeit with heightened volatility, we’ve seen other stock market sectors and asset classes face declines. Bonds fared well as rates fell over the month.

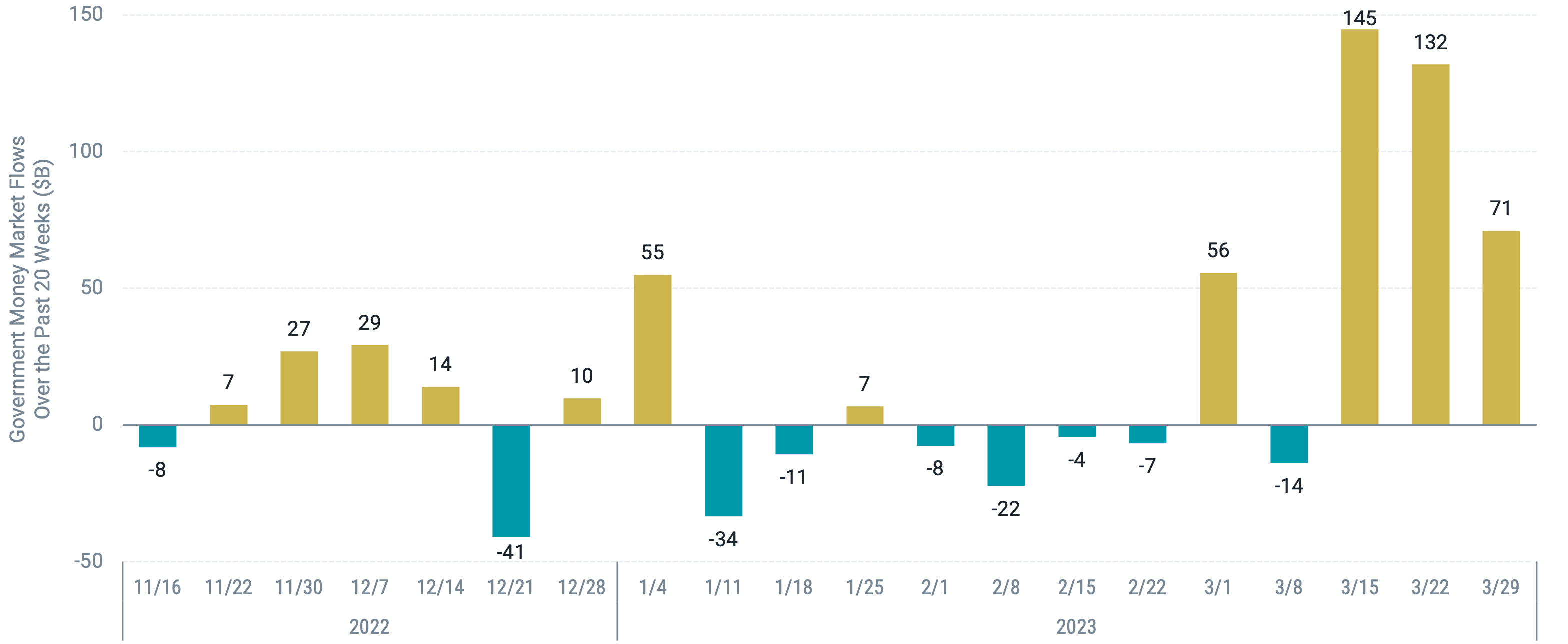

We also see potential evidence of investor anxiety in recent asset flows. Over the three-week period ending March 29, significant dollars flowed into money market funds focusing on government securities. Nearly $350 billion was added over the period, as shown in Figure 3, likely coming from a combination of market investments and bank deposits.

Figure 3 | Significant Dollars Flowed Into Government Money Market Funds Over the Last Three Weeks in March

Data from 11/16/2022 – 3/29/2023. Source: ICI.

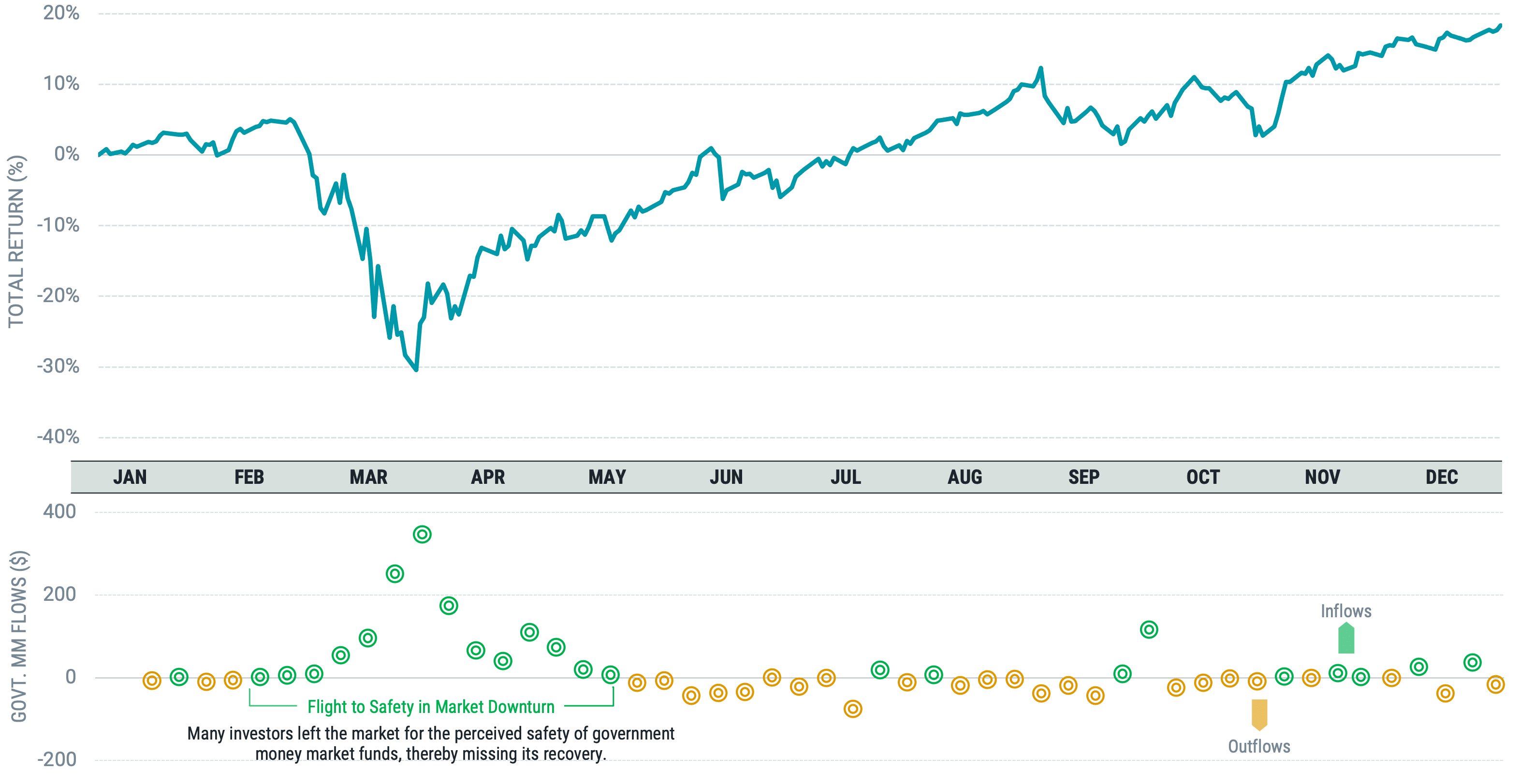

We’ve seen similar behavior before when volatility and uncertainty has spiked. The last time we saw money market flows of this magnitude was in March 2020. As shown in Figure 4, many investors at that time left the market for the perceived safety of government money market funds and may have missed out on the market recovery that followed.

Figure 4 | Money Market Flows and S&P 500 Index Returns Throughout 2020

Data from 1/1/2020 – 12/31/2020. Source: ICI, FactSet, Avantis Investors. Past performance is no guarantee of future results.

This recent example highlights the importance of developing an investment plan adequate for each investor’s risk tolerance, and sticking to it over the long term to avoid selling at times when prices may be depressed by collective anxiety.

It’s fair for investors to feel uneasy about the recent events in the banking industry, but this is only one of many risks and opportunities facing markets today. Among them include how banks approach credit going forward, how that affects inflation and the Fed’s course for interest rates, risk of recession and economic slowdown, geopolitical risks from war in Ukraine and potential conflict between China and Taiwan. The list goes on and on, yet so do markets, which continually assess this information and price securities for positive expected returns going forward.

We believe investors should consider that uncertainty is a part of investing. We see it today, we’ve seen it before, and we’ll see it again. Those that embrace it within a well-diversified, long-term approach are well positioned to ride out the rough times and capture the long-term opportunity of markets.

Endnotes

* References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. As of March 31, none of the funds referenced in this document had exposure to the securities referenced greater than 0.01%.

¹ “Understanding Bank Deposit Growth During the COVID-19 Pandemic.” Board of Governors of the Federal Reserve System. https://www.federalreserve.gov/econres/notes/feds-notes/understanding-bank-deposit-growth-during-the-covid-19-pandemic-20220603.html

Definitions

S&P 500® Index: A market-capitalization-weighted index of the 500 largest U.S. publicly traded companies. The index is widely regarded as the best gauge of large-cap U.S. equities.

An investment in the Funds are not insured or guaranteed by the FDIC or any other government agency. Investments involve risk including the possible loss of principal. Past performance is no guarantee of future results.

This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and, along with other portfolio data, are subject to change without notice.

Diversification does not assure a profit, nor does it protect against loss of principal.

Generally, as interest rates rise, the value of the securities held in the fund will decline. The opposite is true when interest rates decline.